The dream of homeownership often feels like a moving target, especially when the financial landscape shifts as quickly as it has lately. One day you’re ready to sign, and the next, a sudden spike in interest rates makes you second-guess your entire budget. If you have been staring at market charts and wondering if you should pull the trigger or wait for a “better” time, you are certainly not alone. Understanding the current mortgage rates forecast is the key to moving from a state of paralysis to making a confident, informed decision. This guide breaks down the data, the math, and the timing to help you decide if now is your moment.

What is the Current Mortgage Rates Forecast and Why it Matters

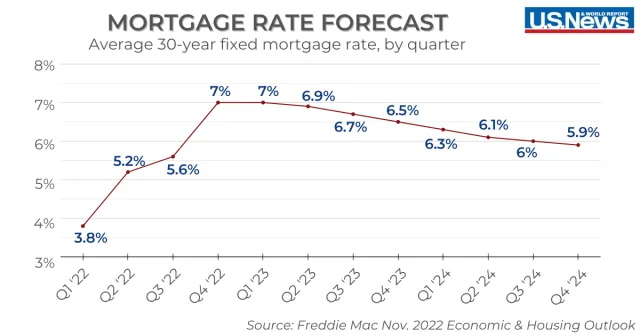

The mortgage rates forecast is an educated prediction of where interest rates for home loans are headed based on inflation data, Federal Reserve policies, and economic growth. For any prospective buyer, these forecasts are more than just numbers on a screen; they dictate your monthly cost of living and your long-term wealth. Even a minor shift of 0.5% can result in paying tens of thousands of dollars more over the life of a 30-year loan.

Why does it matter so much right now? We are in a transitional economic phase. After a period of historic highs, the market is looking for stability. If rates are expected to drop, waiting might save you money. However, if they are projected to plateau or rise due to sticky inflation, buying now could protect you from even higher costs later. Furthermore, mortgage rates directly influence housing demand; when rates dip, competition usually surges, often driving home prices up and canceling out the savings from a lower rate.

Step-by-Step Guide: How to Use Rate Forecasts to Your Advantage

Navigating the market requires a strategic approach rather than just luck. Here is how you can use current forecasts to plan your next move:

-

Track the 10-Year Treasury Yield: Mortgage rates typically follow the trend of the 10-year Treasury note. If yields are falling, mortgage rates usually follow shortly after.

-

Monitor Fed Announcements: While the Federal Reserve doesn’t set mortgage rates directly, their “federal funds rate” influences how much it costs banks to lend money. Pay attention to their monthly meetings.

-

Get Pre-Approved Early: Knowing your “ceiling” allows you to act fast. A pre-approval gives you a clear picture of what a lender will offer you based on today’s specific forecast.

-

Compare “Lock-In” Options: If you find a rate you can afford, ask your lender about a rate lock. This protects you from volatility while you finish your home search.

-

Evaluate the “Cost of Waiting”: Calculate if the potential savings from a lower future rate outweigh the rising cost of home prices during that same waiting period.

The Math Behind Mortgage Rates

Mortgage rates are not pulled out of thin air. They are primarily driven by the Spread, which is the difference between the 10-year Treasury yield and the interest rate offered to consumers.

Historically, this spread stays around 1.7% to 2.0%. For example, if the Treasury yield is 4.0%, a typical mortgage rate would be roughly 5.7% to 6.0%. However, during times of economic uncertainty, banks increase this spread to protect themselves against risk.

The total cost of your loan is calculated using the standard amortization formula:

Where:

-

M = Total monthly payment

-

P = Principal loan amount

-

r = Monthly interest rate (annual rate divided by 12)

-

n = Number of months (e.g., 360 for a 30-year loan)

Even a small change in $r$ significantly impacts $M$ because the interest is compounded over hundreds of payments.

Real-Life Scenarios: Buying Now vs. Waiting

To see how these forecasts apply to your wallet, let’s look at a few practical examples based on a $400,000 loan:

-

Scenario A (Buy Now): You secure a rate of 6.5%. Your monthly principal and interest payment is approximately $2,528. Over 30 years, you’ll pay about $510,000 in interest.

-

Scenario B (Wait 12 Months): Rates drop to 5.5%, but due to high demand, the home price has risen by 5%. Your new loan is $420,000. Your monthly payment is $2,385. While you save $143 per month, you missed out on a year of building equity and paid a higher base price.

-

Scenario C (The Refinance Strategy): You buy now at 6.5% to avoid competition. Two years later, rates drop to 5.0%. You refinance your loan. You effectively “date the rate but marry the house,” securing the property at a lower price and eventually snagging the lower interest cost.

FAQs: Common Questions About Mortgage Forecasts

1. Will mortgage rates go back down to 3%?

Most economists agree that the “3% era” was a historical anomaly driven by the pandemic. Current forecasts suggest that “normal” rates will likely settle in the 5.5% to 6.5% range for the foreseeable future.

2. Should I wait for rates to drop before looking at houses?

Waiting can be risky. When rates drop, many buyers who were on the sidelines jump back into the market, often creating bidding wars that drive prices up faster than the interest savings can keep up with.

3. What is the biggest factor affecting rates in 2026?

Inflation remains the primary driver. As long as the Consumer Price Index (CPI) stays above the Fed’s target, mortgage rates are likely to remain elevated to cool down the economy.

Conclusion

Predicting the exact bottom of the mortgage market is nearly impossible, even for the experts. However, by understanding the current mortgage rates forecast, you can stop gambling and start planning. The “best” time to buy is usually when you are financially prepared and find a home that fits your long-term goals, regardless of minor fluctuations in the news cycle.